As Americans living overseas, we now get the joy of filing two tax returns every year: French and US. While expat taxes can be quite complex, the US-France tax treaty keeps things fairly simple for us.

We’ve now finished our second tax year abroad, finished our US filing, and we’re getting ready to file our first tax return in France in April.

Our tax goal is simple: use our investments to fund our lifestyle without compromise and without paying any income tax.

Disclosure: Some links in this article may be affiliate links. If you choose to use them, we may earn a commission at no additional cost to you. We only recommend services we believe are genuinely useful.

The Tax Appeal of France

Why the US isn’t tax-free

Retiring in the US and not paying income tax is fairly straightforward: use the large standard deduction and generous 0% capital gains bracket to cover all spending needs.

But things get more complicated for early retirees like us, who would depend on the ACA for healthcare. While we may not pay federal income tax, having our ACA premiums tied to our gross income creates an effective income tax.

The more money we roll from 401k to Roth, the higher our healthcare premiums go. Even if we can’t touch that money for five years.

France solves this problem

France decouples healthcare from income for retirees. Below a capital income of €48,060 in 2026 for a couple (50% of the PASS value per person), there are no additional taxes or charges for healthcare, at least not yet.

With the US-France tax treaty protecting US-sourced capital income from French taxes, the same strategy of using the standard deduction and 0% capital gains bracket can be used, but without healthcare costs rising with income.

Our US-France Tax Strategy

Regardless of our income needs for the year, our goal is to realize as many capital gains as possible and withdraw as much from our 401k’s as we can, all while paying a 0% tax rate. We have three limits to avoid while tax residents of France:

- The standard deduction of $31,500 in 2025

- The 0% capital gains bracket of $96,700 in 2025

- The French CSM charges above €47,100 in 2025

Because the 0% capital gains bracket is so much higher than the French CSM limit, we can ignore it.

Our standard deduction bucket is filled first with interest, non-qualified dividends, and any short-term capital gains. The leftover amount is then used for our Roth Conversion Ladder, where we roll money out of our 401k’s and into our Roth IRAs.

Our French CSM bucket is first filled with interest and dividends from our after-tax accounts. We fill it the rest of the way up by selling investments in our after-tax account and realizing the gains.

We only spend about $60,000 per year, but this strategy generates much more income. We simply reinvest what is leftover at a higher cost-basis; essentially a wash sale, but with gains instead of losses.

Filing Our US Taxes as Expats

Last tax year, we successfully used the FEIE to avoid paying US income tax by traveling outside of the country for 11 months while working remotely, but not establishing tax residency in another country.

This year, we’ve established tax residency in France and must file French taxes by May. Because we don’t expect to owe any taxes to either country and won’t need to take the Foreign Tax Credit, we finished our US taxes early.

Filing for free with FreeTaxUSA

Because our filing was very simple with just a few 1099’s, we used FreeTaxUSA. We maintain a virtual mailbox in the US, which we use for our tax return. FreeTaxUSA supports foreign mailing addresses, however not foreign phone numbers. We kept our old US numbers through Google Voice, so not an issue for us.

We’ve also used OnLineTaxes before and they’ve been fine, and are often recommended as a good alternative for expat tax returns. Their website, however, is not accessible from outside the US and requires a VPN to access from France.

Why we always choose a free option

We always strive to use free tax filing software, and hope you’ll consider it too. Profits made from Turbo Tax and other paid software go towards lobbying the US government to keep tax filing complicated and the US taxpayers dependent on expensive yearly software.

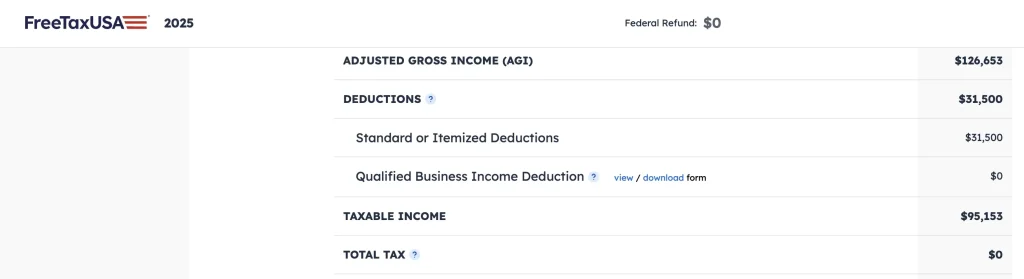

Our US tax filing – almost perfect

All of our careful cost basis tracking, qualified dividend estimation, and interest rate forecasting really paid off. We glided in just $150 below our tax-free limit and got that sweet $0 refund notification.

We only had one mix-up – we missed the announcement from Trump’s OBBBA in July raising the standard deduction from $30,000 to $31,500. We missed out on $1500 of 401k rollovers by not double-checking our assumptions in December, but at least we didn’t owe anything.

Looking Forward to French Taxes

Now that our US tax returns are out of the way, we can prepare for our first French tax filing in April, and we will receive a bill for the CSM charges in November. We already submitted Form-2043 in January, in the hope of receiving a tax number and setting up our profile online. But it seems all first-year residents are expected to file a paper return regardless.

As odd as it may sound, we’re actually looking forward to filing our French taxes. A huge driving factor behind the creation of this site was the lack of real-world examples of Americans filing both US and French taxes and writing about their experience with the tax treaty online.

Will This Zero-Tax Situation Last?

Live in France and pay no taxes? It’s almost too good to be true. After all, France has one of the highest tax rates in the world.

The US-France tax treaty provides a high amount of protection, and it would take a two-thirds majority in the US Senate to change. But there’s been a growing sentiment in France about Americans paying their fair share.

If we expected this situation to last, we wouldn’t feel the need to realize as many capital gains as possible, nor to roll over as much of our 401k’s as we possibly can. We’re doing this now with the expectation that the gravy train will eventually end.

France already has some fairly nasty ways of getting at your money, with or without the treaty. We want our cost basis to be as high as possible before any new surprise tax legislation gets passed and retroactively applied, or the US is deemed to be a non-cooperative tax country.

Questions? Comments? We’d love to hear from you in the comment section, or feel free to write us directly.

🥖 🧀 🍷

Subscribe to our Newsletter and never miss a post!

Leave a Reply